Despite a 26% drop in underlying profit for fiscal year 2025, BHP delivered a dividend beat that sparked a positive market response. The mining giant has shown resilience—and made clear where its confidence lies.

The Financials—Strong Payout, Slimmer Bottom Line

BHP announced a final dividend of US$0.60 per share, bringing the total annual payout to US$1.10—its highest since 2017 and comfortably above analyst expectations. That results in a 60% payout ratio, signaling commitment to shareholder returns. Meanwhile, overall profit slid to US$10.16 billion, the lowest in five years, driven mainly by weaker iron ore and coal prices

The market seemed to embrace this balance of caution and generosity, with BHP’s shares rising over 1% on the day. Analysts from Citi noted that “we expect the higher div payout ratio to be taken as a modest positive”, highlighting how the dividend helped overshadow the earnings dip.

Strategic Confidence: Payouts, Growth, and Expectations

CEO Mike Henry spoke to the firm’s strength in key markets and commodities:

“We remain confident in the long-term fundamentals of steelmaking materials, copper and fertilisers… BHP is well-positioned to deliver enduring value through the cycle.”

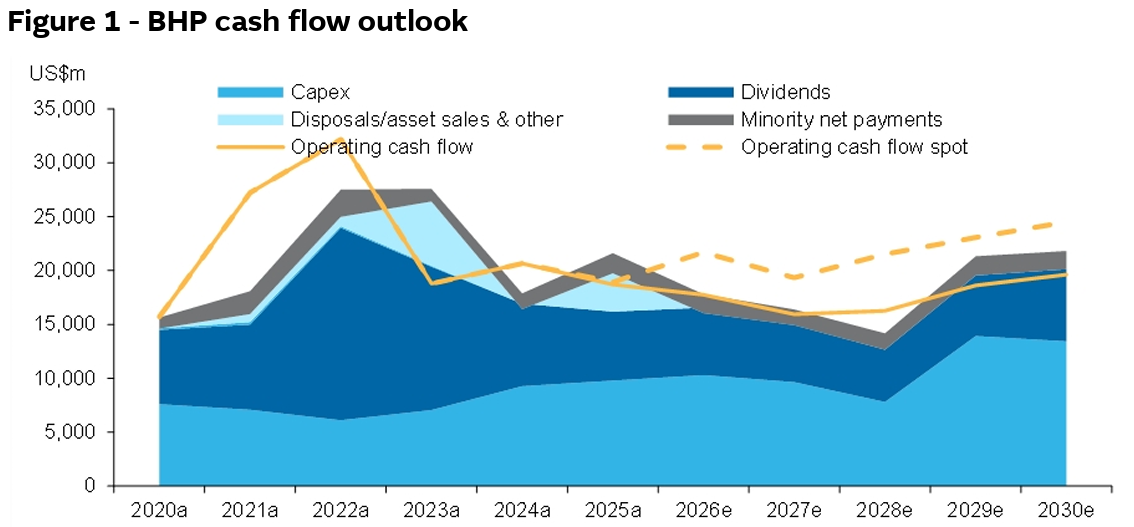

BHP also raised its net debt target range to US$10–20 billion, up from US$5–15 billion, enabling investment in organic growth projects.Over the next two years, the company plans to spend US$11 billion annually on capital and exploration—beating its FY24 spend of US$9.8 billion—before settling at around US$10 billion per year by FY2028–30.

Challenges Ahead: Coal Pressures and Strategic Shifts

On the ground in Queensland, BHP faces pressure from “extreme” coal royalty rates—reportedly translating to effective tax burdens over 60%. CEO Henry warned the company may consider pausing low-margin operations if prices don’t recover.Meanwhile, earnings from coal declined sharply, but were offset by stronger copper results—which delivered a 44% jump in earnings, making it a growing focus.

Summary Snapshot

| Key Metric | Detail |

|---|---|

| Underlying Profit | US$10.16 billion (–26%) |

| Final Dividend / Total | US$0.60 per share / US$1.10 total |

| Payout Ratio | 60% |

| Net Debt Target | Raised to US$10–20 billion |

| CapEx Guidance | US$11 billion annually for next 2 years, then ~US$10 billion post-2028 |

| Tactical Concerns | High coal royalties; potential Qld operational pauses |

| Strengths | Record copper earnings; diversified portfolio |

Bottom line: BHP’s upward-dividend surprise amid softer earnings sends a confident message: the company is betting on sustained commodity demand and strong cash flow—even through cyclical turbulence. The increased payout and bold CapEx outlook signal that BHP sees its diverse portfolio and balance sheet as foundations for long-term value creation.