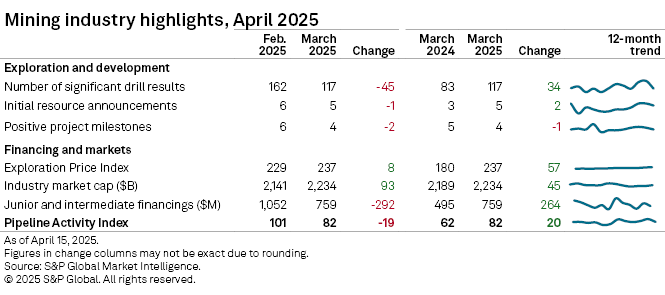

The mining world awoke in 2025 with a renewed sense of promise. Early indicators show that exploration is surging forward, particularly in gold and base metals, as key performance metrics point upward. While still below its late-2024 highs, the industry seems to be regaining its footing—and maybe even building momentum.

Trends That Signal Growth

According to data tracked by S&P Global, the Pipeline Activity Index (PAI) climbed 5% in January, reaching a respectable 85—just shy of its October 2024 peak of 98. Notably, gold-related activities posted an impressive 8% gain, while base metals saw 3% growth.

Drilling activity also saw meaningful upticks: total projects rose 17%, with drill holes increasing 2% compared to December. More specifically:

- Early-stage exploration projects surged by 31%.

- Mine-site drilling expanded 27%.

- Late-stage project activity climbed 4%.

While these numbers remain lower year-on-year (down 6% and 1%, respectively), they reflect a turning point—especially in the earliest phases of discovery.

Project Highlights Bring Early Wins

Some standout successes emerged alongside the broader data. In Morocco, Aya Gold & Silver’s Zgounder mine yielded an astonishing 21 meters at 2,165 grams per ton of gold—a rare and promising intersection.

January also saw a rise in initial resource announcements (six in total, up from four in December), with three tied to gold projects. Among them, Minsud’s Chinchillones Complex in Argentina stood out for its copper-rich potential.

The month also brought seven major milestones—one more than December—including first gold pour at Artemis Gold’s Blackwater mine, a feasibility study wrap for Ghana’s Bibiani extension, and the launch of construction at Alamos Gold’s Lynn Lake site.

Financial Backdrop: Strong Markets, Tight Funding

Metal markets gave exploration a lift in January: gold prices rose 2.5%, along with gains in copper and platinum. Nickel and cobalt lagged behind. Overall, mining company valuations climbed 2.4% to reach US$2.13 trillion.

Still, funding remains constrained. Exploration budgets took a dive—aggregate financing dropped 48% to US$463 million, the lowest monthly total in three years. Notably, gold-specific financing plunged 59% to US$153 million, with just 56 deals recorded and only a single fundraising event exceeding US$50 million.

“We’re seeing excavation enthusiasm return, but tight capital markets continue to bite,” commented one industry veteran. “The real challenge will be turning renewed exploration energy into funded, forward motion.”

Snapshot—January 2025 Mining Exploration

| Metric | Change vs. Previous Period |

|---|---|

| PAI Score | +5% (to 85) |

| Total Projects | +17% |

| Early-stage Exploration | +31% |

| Mine-site Drilling | +27% |

| Late-stage Projects | +4% |

| Market Cap | +2.4% (~US$2.13 trillion) |

| Financing Volume | –48% (~US$463 million) |

| Gold Financing | –59% (~US$153 million) |

Bottom line: The mining landscape for early 2025 is shaping up to be one of cautious optimism. Exploration is ramping up, results are promising, and valuations are buoyant—but funding remains a bottleneck. The industry needs capital flows to match its ambition if the trend is to continue beyond this early burst of energy.